(Why a complete financial plan needs both)

Let’s start with a fact we can all agree on: Your CPF Ordinary Account (OA) is an excellent Safety Net. It provides a risk-free 2.5% return that offers stability in an uncertain world.

It does exactly what it was designed to do: Preserve your capital.

For many of us, this Safety Net has a vital job: Securing our Home. If you are using your OA to pay a mortgage or save for a downpayment, your Safety Net is working perfectly.

However, stability comes with a trade-off. The role of a Safety Net is preservation, not maximization. For long-term wealth accumulation, you need a different tool.

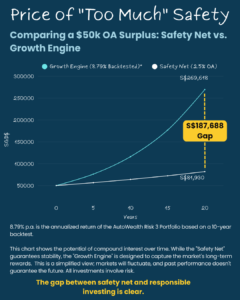

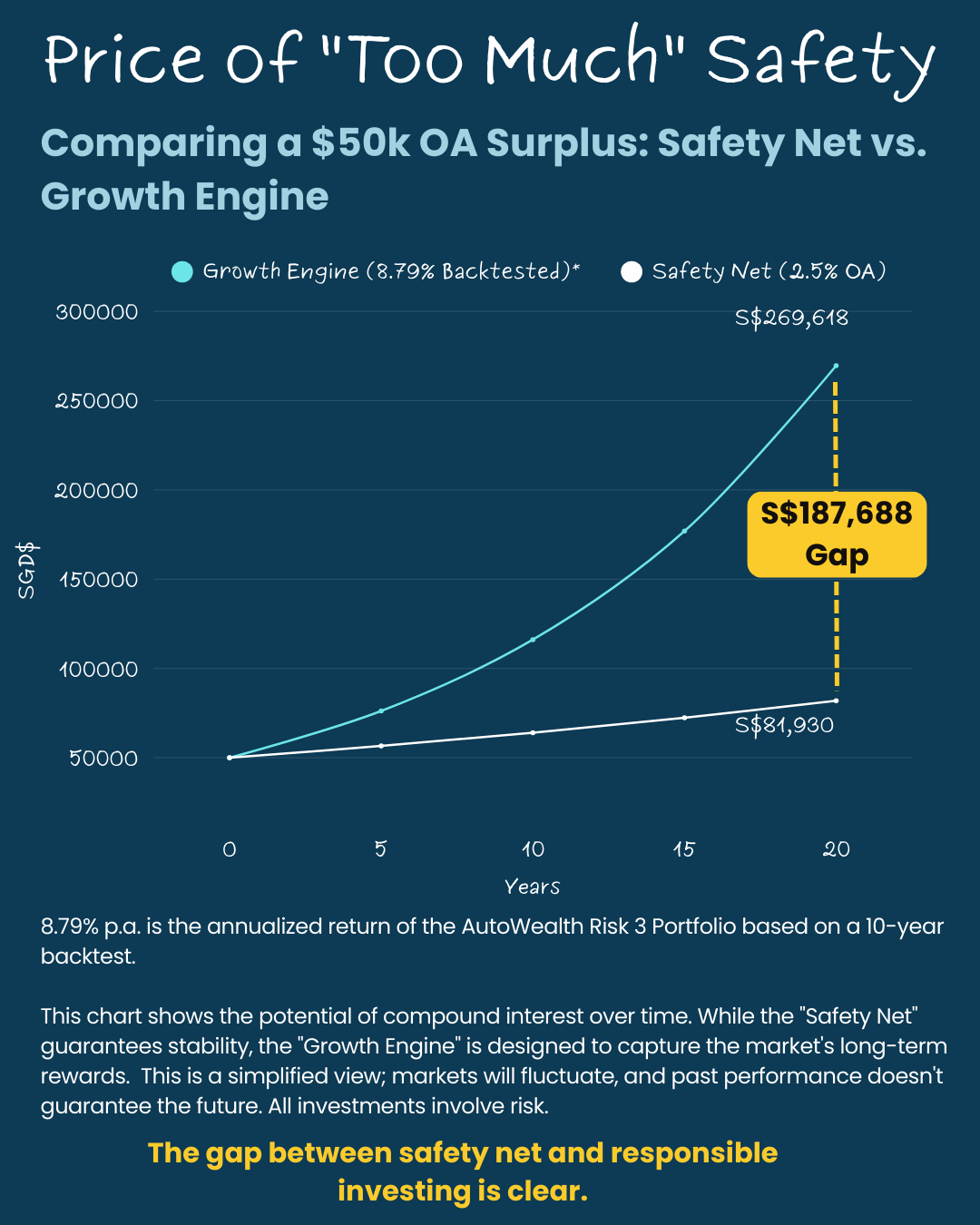

The Price of "Too Much" Safety

If you have surplus OA funds—money truly not needed for housing—leaving it all in the Safety Net means missing out on the compounding power of the global markets.

How big is the difference? Let’s look at the numbers.

Let's compare a $50,000 surplus kept in the OA versus deploying it into a diversified global portfolio (based on the 10-year backtested performance of AutoWealth's Risk 3 portfolio).

| Strategy | Return Rate | Outcome (20 Years) |

|---|---|---|

| Safety Net (OA) | 2.5% (Risk-Free) | $81,930 |

| Growth Engine | 8.79% (Backtested*) | $269,618 |

| THE DIFFERENCE | +$187,688 |

That is not just a number. That is a potential $187,688 difference.

Are You Ready to Build Your Growth Engine?

Investing your CPF is not for everyone. It depends entirely on your life stage. Find yourself below:

Phase 1: The Homebuyer (Priority: Clarity)

This is the most critical phase. Which camp are you in?

- Camp A: Does your existing mortgage currently wipe out your entire monthly OA contribution? Your OA is doing its job perfectly. Do not invest.

- Camp B: Are you planning to buy your home in the next 3–5 years? Pause & Consult. While you can invest (our portfolios allow withdrawal at any time), investing with a short timeframe involves higher risk. Speak to your assigned AutoWealth wealth manager first to ensure this matches your specific risk appetite.

Phase 2: The Accumulator (Priority: Efficiency)

Has your income grown? Is your monthly OA contribution now consistently higher than your mortgage payment? You have turned the corner. That monthly "excess" is your new surplus. Consider giving it a job in your Growth Engine.

Phase 3: The Optimiser (Priority: Freedom)

Is your home paid off? Or did you intentionally pay in cash to keep your OA free? You are in the prime position. Because your funds have zero housing liability, your entire balance is surplus. You have the maximum capacity to capture the "Growth Engine" advantage.

A Critical Note: Prudence over Speculation

If you are in Phase 2 or 3 and you are ready to do more with your OA surplus, remember this rule: Do not chase returns blindly.

Your CPF is your retirement lifeline. It is not for speculation. High Growth Equity is rarely the answer: Taking maximum risk to chase the highest possible number is dangerous for retirement funds.

The "Sleep Well" Standard: The goal is not to beat the market at all costs; it is to beat the Safety Net (2.5%) while staying within a risk level that lets you sleep at night.

We believe the correct approach is a risk-adjusted portfolio—one that is globally diversified and tailored to your specific timeline, ensuring you capture growth without gambling your future, such as those we have on our AutoWealth platform.

The Decision

If you have the OA surplus, you have a choice. You can keep it all in the Safety Net for preservation, or you can activate a portion to build the Growth Engine you deserve.

*Disclaimer: The 8.79% p.a. figure represents the annualized return of the AutoWealth Risk 3 portfolio based on a 10-year backtest, not actual historical trading results. All investments involve risk. Past performance—including backtested data—is not indicative of future results, and projected returns are not guaranteed. This chart is for illustrative purposes to show the power of compounding over the long term. It is a simplified view and does not reflect the actual short-term volatility (price fluctuations) of investment assets, which can be significant. Investment value can go down as well as up.