From the Desk of Ow Tai Zhi, CEO

Following our update on the "Growth Engine", the most common question I received was the logical next step: "I want to grow my CPF, but how much should I invest?"

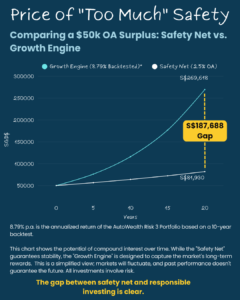

It is the most important question you can ask. You view your OA as a safety net for your home—and you are right. You should never risk money you need for near-term security.

The "Smart Buffer" Framework

I want to share the stress test we use to help you identify your Investable Surplus. This ensures you can earn higher market returns without ever risking your family’s housing needs.

To find your safe number, simply compare two figures. You should reserve the HIGHER of the two:

- The CPF Requirement: CPF Board requires the first S$20,000 of your OA to be set aside and earn extra interest.

- The Safety Check: Calculate 12 months of your share of the mortgage payments.

A Real-Life Example

Let’s look at a scenario common among our clients (e.g., paying for a 5-Room flat or EC) in a modern dual-income household.

THE STRESS TEST

Verdict: Since the mandate ($20k) is higher than safety needs ($18k), your "Regulatory Floor" covers your safety buffer.

"I have a Surplus. How do I start?"

If the math works, the next step is administrative. To invest your OA savings, you need to have a CPF Investment Account (CPFIA) with a local bank.

If you do not already have one, it takes 5 minutes to open via your bank app. You do not need to visit a branch.

Your Action Plan

- Run the Math: Do you have an "Investable Surplus"?

- If YES: Open your CPFIA via your bank app today (takes ~3-5 days), if you do not have one.

- Link & Lock: Once approved, link it to AutoWealth to lock in your 0% Advisory Fee on CPF investments.

(Important) Buying a home soon?

If the "Buffer Math" shows you need every cent for a downpayment, do not invest. Your priority is liquidity. However, you can still reserve your 0% CPF Advisory Fee Waiver for the future.

We will tag your account as "Eligible" so you can use it when you are ready (valid until 2030).