Holdings of equity constitute the core of most institutional and individual portfolios for theoretical and practical reasons. The expected return characteristics of equity instruments satisfy the need to generate substantial portfolio growth over the long-run.

Equity Risk Premium

Equity risk premium is defined as the incremental return to equity holders for accepting risk above the level inherent in fixed income investments.

Equity investments promise higher returns than fixed income investments in the long-run, although in the short-run, the prospect of higher returns sometimes remain unfulfilled.

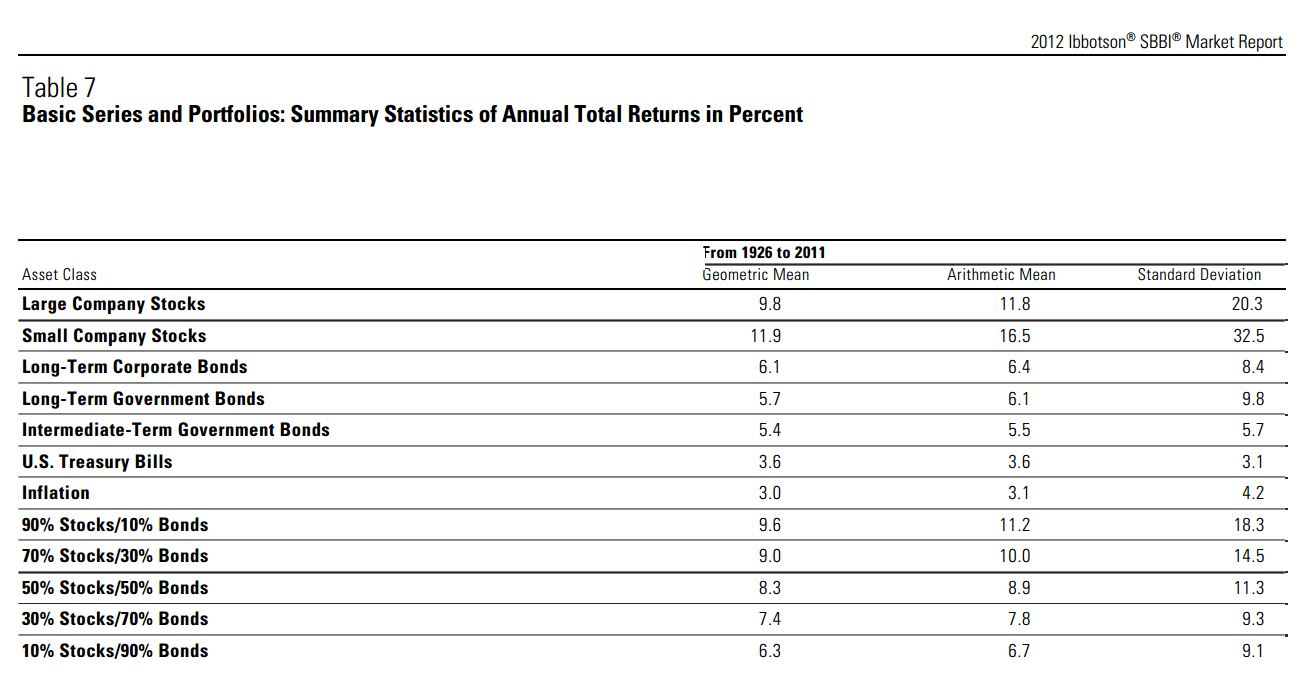

Morningstar produces a widely used set of capital market statistics that reflect equity-and-fixed income return differential of 4.4% per annum between 1926 and 2010, indicating that equity holders enjoyed a substantially higher return over fixed income holders. Finance theory and capital markets history provide analytical and practical underpinnings to the notion of an equity risk premium. In the absence of higher expected returns for fundamentally riskier equity, investors would totally shun equity for lower-risk fixed income. Equity risk risk premium must exist for capital markets to function effectively.

Equity Characteristics

Equity exhibits a number of compelling characteristics.

Inflation Hedge – Equity tend to provide protection against unexpected increases in inflation in the long-run. The positive long-run relationship between equity prices and inflation stems from rational behavior, as investors weigh and arbitrage the costs of acquiring assets in the real economy vis-a-vis the costs of acquiring similar assets on equity markets.

In the short-run, the protection can be unreliable at times when irrational investors respond to unanticipated inflation by increasing the discount rate applied to future cash flows without adjusting those cash flows for the increases in inflation.

Alignment of Interest – The general alignment of interests between corporate managers and shareholders bodes well for equity investors. In most instances, corporate executives benefit from enhancing shareholder value, serving the financial goals of management and investors alike. For example, corporate executives often share in gains associated with greater corporate profitability, indirectly through increased compensation and directly through increased values for personal shareholdings.

Unfortunately, there are instances where agency problems can occur when management (agents) benefit at the expense of shareholders (principals). The most common conflict of interest between shareholders and management stems from compensation arrangements for management. High levels of salary and benefits accrue to management regardless of the level of underlying corporate performance. Because larger companies provide better compensation packages than smaller companies, corporate managers may pursue corporate growth simply to achieve higher levels of personal earnings regardless of the impact of corporate size on profitability.

One way to reduce the conflict involves ownership of stock by corporate management. Savvy investors seek companies with high levels of insider ownership.

Liquidity – Equity trades in broad, deep, liquid stock markets, affording investors access to an impressive range of opportunities. According to the World Bank, the U.S. equity market boasted assets in excess of US$18.6 tillion as at 2012, making it the largest liquid capital market in the world.

The Need To Diversify

Despite the compelling characteristics of equity as an asset class, investors must guard against over-concentration of equity in an investment portfolio. Returns of fixed income and cash may exceed returns of equity during particular years. For example, from the market peak in october 1929, it took equity investors twenty-one years and three months to match returns generated by fixed income investors.

In summary, asset allocation to equity should remain a starting point for most investment porfolios. However, a fine balance must also be drawn given the shortcomings of equity in the short-run.