Here’s a thought: you, in ten years, moving out of your 4-room HDB and into a terraced house, downpayment done and dusted. Sounds like a dream? We’ll show you how its closer to reality than you think.

Let’s lay out the facts. A terraced house located in the East of Singapore currently costs around S$ 2.5 million. However, due to inflation, you will more likely be facing a heftier S$ 3.1 million in 10 years. To afford this terraced house, you’ll have to overcome two hurdles: (1) 25% downpayment, and (2) monthly instalments.

Downpayment

25% downpayment translates to S$ 780,000. And let’s not forget the stamp duty, which works out to be around S$ 110,000. So your downpayment is actually close to S$ 890,900.

A sharp reader will realise that you don’t actually have to pay all S$890,900 straight out of your pocket (although MAS mandates you pay a quarter of it fully in cash). You’ll have your HDB proceeds and CPF savings.

But will they amount to S$ 890,000? Our calculations say no. Let’s quickly run through each source of funding:

- HDB proceeds. They won’t actually help as much. Let’s assume you bought your 4-room resale at the median price of S$ 470,500. In ten years, you should be able to sell it at S$ 608,850. After deducting your outstanding mortgage loan with HDB, agent proceeds at 2% of sale price and repaying your CPF with interest accrued, you might actually end up with a deficit of about S$ 20,000. Let’s assume in this case you breakeven.

- CPF funds. A great deal of your HDB proceeds end up here as you have to return the money you “borrowed” for your HDB. Hence, your CPF funds will help to offset a big bulk of the downpayment. Here’s the catch: 5% of the downpayment has to be paid strictly in cash, and you have to leave the basic retirement sum untouched. Assuming you and your spouse earn the median Singaporean salary, both of you can use a combined S$ 417,000 to pay for your landed property.

And the remaining $ S473,000? You’ll have to fund it in cash. Here, we present two scenarios.

The first: You save. If your household saves S$ 3,000 per month for the next ten years, you’ll have S$ 360,000 in cash savings. You’re still short of S$ 113,000.

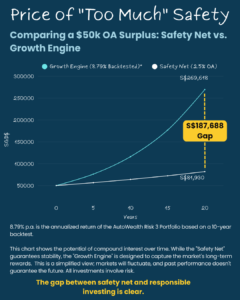

The second: You invest. You invest the same S$ 3,000 into an investment portfolio every month. For illustrative purposes, we’ll assume your portfolio yields approximately 6% returns per year, net of all fees. And yes, 6% returns, net of all fees, is entirely achievable (see below).

The easiest way to consistently get 6% returns is to do it through a robo-advisor. For instance, AutoWealth.

Based on robust back testing, a moderate risk portfolio can achieve 6.2% annual returns, across an investment horizon of at least 3-5 years.

If we look at actual performance, the same portfolio has been raking in 7.6% annualised returns from May 2016 to June 2018. Bottom line: 6% returns is easily achievable.

After 10 years of reaping 6% returns per year, you will have accumulated approximately S$ 503,000. That’s S$ 29,000 in excess for your downpayment. But never too little to help with your monthly instalments.

Monthly instalments

After factoring in partial repayment from your excess investment earnings and your subsequent monthly CPF Ordinary Account contributions, your household will have to shoulder approximately S$ 7,000 a month.

This figure may seem daunting, but don’t forget that you and your spouse will be at the peak of your careers! A combined household income of S$ 14,000 – S$ 16,000 is sufficient to comfortably sustain a S$ 7,000 monthly instalment. Say both of you hit a position of senior manager or higher. A combined income of S$ 20,000 is entirely within reach.

So, work hard, but don’t forget to make your money work harder for you! Start putting your money to work for your 10 year plan today!!

References: HDB, data.gov (HDB and landed resale index), URA, MOM, MAS, CPF calculators