Reflections on AutoWealth’s Recommendations and Portfolio Performances

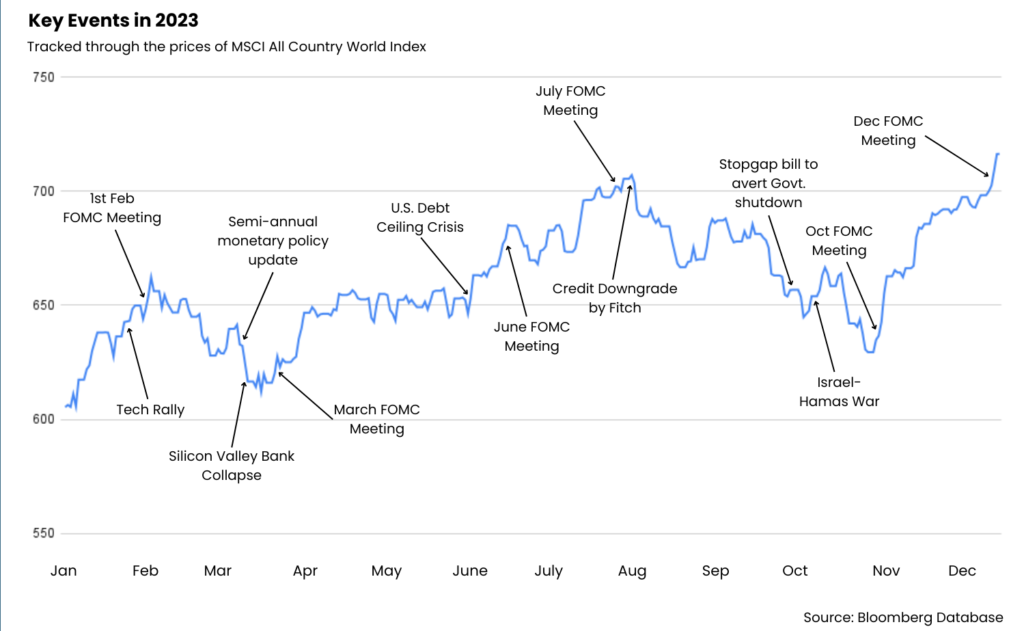

2023 has been an eventful year for financial markets – from a mega-cap tech stock surge, bank failures to a long-awaited end of the rate hike cycle. To help investors navigate through significant market events, AutoWealth published market commentaries and recommendations for our clients from time to time through our telegram community. As the curtain draws on 2023, we reflect on our recommendations and AutoWealth portfolio performances. To provide reference points, we used the MSCI All Country World Index to track major events and their effects on the market.

Fed Signals End of Rate Hike Cycle and Potential Rate Cuts in 2024

U.S. Monetary Policy

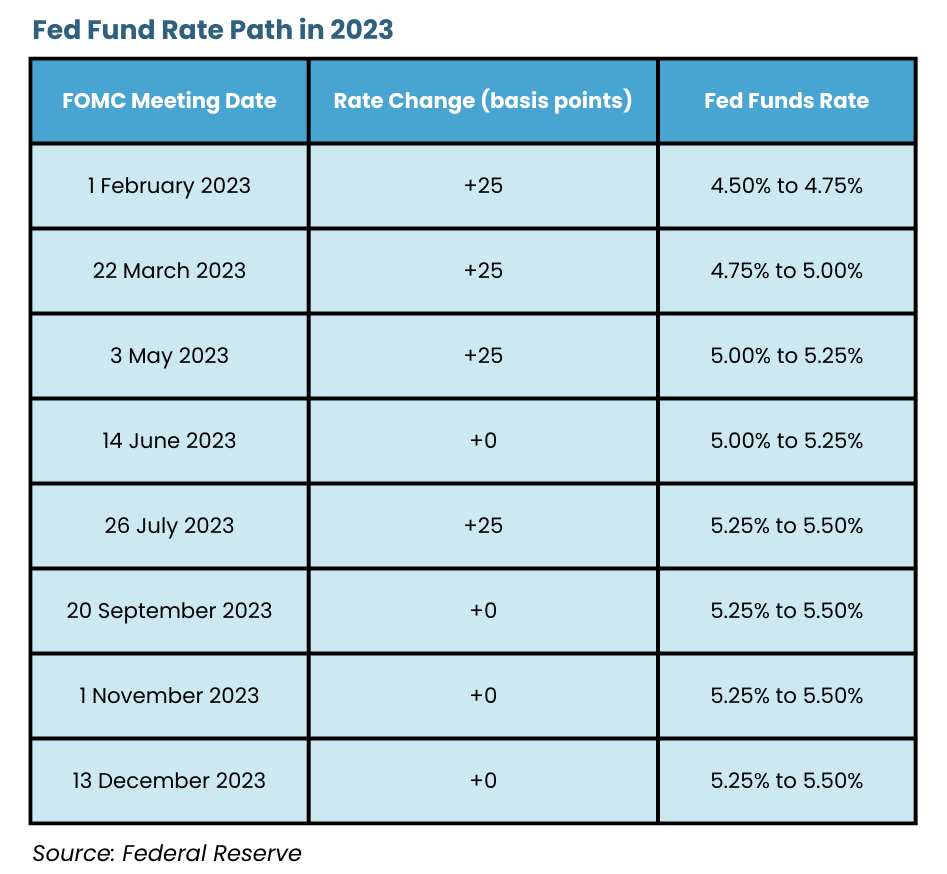

Over the past 2 years, the Fed’s monetary policy went through a slew of adjustments and now, the Fed finally feels confident to call the end of its rate hike cycle and start discussions for rate cuts in 2024. As shown in the table below, Fed fund rates were raised 4 times earlier this year to tame inflation, before keeping steady at a restrictive level since the September FOMC meeting for disinflation to take hold. While global markets tend to be volatile at key data and policy announcement dates throughout the year, stocks and government bonds markets seem to be enjoying an early Santa rally with a soft-landing well in sight.

AutoWealth’s Note:

In our 2023 market outlook published on 25 December 2022, we reiterated our house views that “Inflation is cooling off as per the wishes of the Federal Reserve and positive economic growth suggests the economy is solid & nowhere near a recession. This best of best worlds shouldn’t be greeted with markets selling. And when there are such irrational disconnections, investment opportunities present themselves.” In our 23 March 2023 commentary, we highlighted again that “Investors should consider being adequately invested as markets navigate into a new monetary cycle that is positive for stocks and bonds investments.” Clients, who heeded our call and remained invested since 25 December 2022 and 23 March 2023, would have yielded 16.3% and 13.1% returns respectively.

China’s Re-opening after Covid: A Promising Start, but Challenges Ahead.

On 27 December 2022, China announced an end to its quarantine requirements for inbound travelers starting 8 January 2023, marking a fundamental shift from its stringent zero-COVID policy upheld for almost three years. This move marks the reopening of the second largest economy, which many economists expect to see a strong consumption rebound, and in turn drive global economic growth.

Autowealth’s Note:

Hopes were high, and the pivot in policy led to a strong but brief rebound in China’s economic activity, fuelling a 7.1% gain in global markets in the first month of January 2023. However, in the second quarter, China’s recovery lost momentum as it faced several headwinds from an adverse geopolitical and economic environment and overlapping domestic structural challenges including widespread defaults in the real estate sector which accounts for one-quarter of its GDP. Despite China rolling out a series of measures to stimulate the economy, we believe weak consumer demand and its deepening property crisis will continue to drag on growth.

The Rise of Mega-Cap Tech Stocks: A Tech Rally Fueled by AI and “Flight to Safety”

The rally this year was largely driven by mega-cap technology stocks, with the MSCI World Information Technology Index outperforming the MSCI All Country World Index. The tech rally was fuelled by several factors including growing interest over artificial intelligence-related (AI) stocks and a “flight to safety” towards mega-cap names with cash-rich balance sheets.

Autowealth’s Note:

Our AutoWealth Plus+ Future 2050 portfolio, with 58.9% target allocation to the technology sector, benefited from the tech rally, registering a 28.6% return year to date as of 15 December 2023.

In addition, amid the growing demand of Artificial Intelligence (AI), its vital role and long-term potential in a digital economy, we have included 2 new ETFs [VanEck Semiconductor (SMH) and First Trust Nasdaq Artificial Intelligence and Robotics (ROBT)] in our Future of Digital Economy Portfolio as of 25 October 2023. Investors who feel strongly about the AI macro-trend, can consider the Future of Digital Economy portfolio, which offers more focused exposure to AI and digital sectors.

Banking Sector Turmoil: A Tale of Turmoil and Market Shockwaves

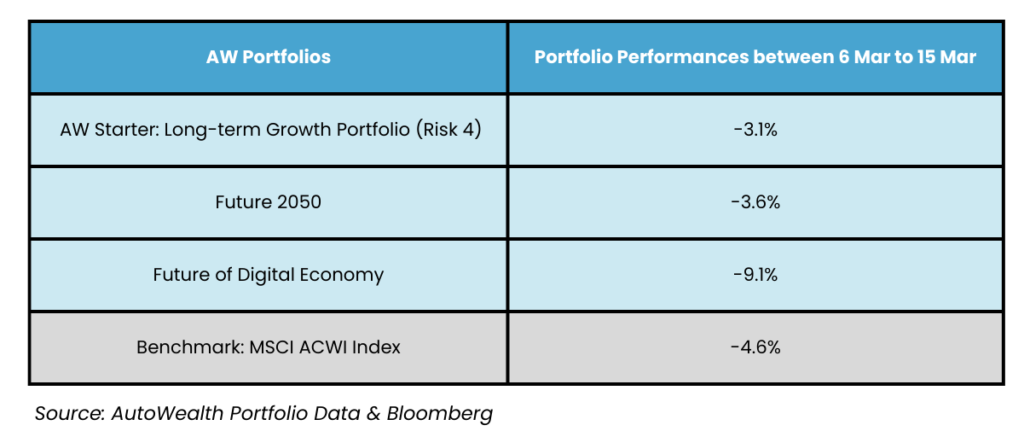

In March 2023, we witnessed the collapse of Silicon Valley Bank, Silvergate bank, Signature Bank and the US$3.2 billion takeover of Credit Suisse by UBS unraveled one after another in the span of 11 days, sending shockwaves to the global financial system. While the fundamental reasons for failure vary across each bank, equity markets overall declined 4.6% through the banking turmoil from 6 to 15 March 2023.

AutoWealth’s note:

In our 12 March 2023 commentary, we highlighted minimal exposures of our portfolio towards SVB and the downstream companies affected, reassuring investors that our portfolios are significantly defensive due to our robust diversification approach. Indeed, compared to the 4.6% drawdown in the MSCI ACWI Index, our portfolios faced a relatively smaller dip as seen in the table below. The exceptional -9.1% plunge in the Future of Digital Economy portfolio was mainly due to the decline in both Internet and e-commerce stocks, which were affected by the Coinbase Inc and Binance’s temporary suspensions of USD coin conversions and Peloton Interactive Inc’s loss in a patent infringement suit.

Looming Danger of the U.S. Debt Ceiling: U.S. Debt Default Threatens Economic Stability

The U.S. was reported to be at risk of default as soon as 1 June 2023 if the U.S. House & Senate could not reach an agreement to raise the debt ceiling. Debt ceiling is the maximum limit that the U.S. can borrow by issuing treasury debt (bonds). The debt ceiling has been raised 78 times since the 1960s.

AutoWealth’s note:

In our 30 April 2023 commentary, we highlighted that “Lawmakers understand a default would send shockwaves on the economy and cause irreparable damage to the U.S.’s credit & international standing. The U.S. is simply too big to fail.” As such, clients are advised to “mentally prepare to welcome any material pullback, if it occurs, with open arms” and to capitalize on this opportunity by making investment top-ups. Albeit the mild pullback, clients who heeded our call, would have locked in a 1.3% market discount.

Downgrade of the Pristine U.S. Credit Rating

After being downgraded by Standard & Poor from AAA to AA+ in 2011, the U.S. was placed under negative rating watch by Fitch in May 2023 and subsequently downgraded from AAA to AA+ on 1 August 2023. This move is primarily due to the political impasse over management of the country’s debts, their constant 11th hour resolutions and lack of a robust fiscal framework. In reaction to the credit rating downgrade, equity markets declined 5.7% between 31 July and 18 August 2023.

AutoWealth’s note:

In our 2 August 2023 update, we highlighted that there will be “material but insignificant short-term drag” given that markets have already priced in the possibility of a downgrade. “Any pullbacks would present buying opportunities for investors.” Clients, who heeded our advice, would have locked in a 0.9% market discount.

Looming Danger of a U.S. Government Shutdown

In September 2023, there was considerable concern surrounding the looming possibility of a U.S. government shutdown as the 30 September 2023 deadline to agree on spending bills edges closer. Disagreements between the Democrat-controlled Senate and the Republican-controlled House elevated the risk that the Congress will fail to pass legislation for funding the government before the imminent deadline to avert a shutdown. Eventually on 29 September 2023, both the House and Senate successfully passed a 45-day funding bill, temporarily averting the shutdown and calming financial markets. Amidst the shutdown fears, equity markets declined 5.5% between 14 September and 2 October 2023

Autowealth’s Note:

We warned investors that fears of a potential government shutdown would add to market volatility. In our 27 September 2023 update, we shared the following: “As the U.S. partial government shutdown situation is still developing, you may wish to consider investing part of the idle cash now, whilst reserving the remaining idle cash in case of potentially lower market price levels”. Though the bill’s passage has limited the duration and magnitude of the discounted opportunities, clients who heeded our call would have locked in a 2.0% market discount.

The Israel-Hamas War

Following the outbreak of the Israel-Hamas conflict on 7 October 2023, financial markets remained relatively calm in the initial few days. In the subsequent 3 weeks, while markets declined 2.9%, it did not trigger a market panic characterised by a more than -5% decline seen in previous historical armed conflicts.

Autowealth’s Note:

In our 30 October 2023 update, we expressed our house views on the conflict: “We believe the probability of escalating whilst cannot be ruled out, is relatively low at this point. Consequently, we believe downside risk is limited. Also worthy to note, markets will contend with the Fed rate pause, strong corporate earnings, continuing progress in disinflation, which are providing support for upside.” As forecasted, our AutoWealth Starter portfolio experienced a modest 2.9% decline from 7 to 27 October 2023, and was followed by an upward trend as financial markets shifted its focus to a more dovish Fed in the November 2023 FOMC meeting.

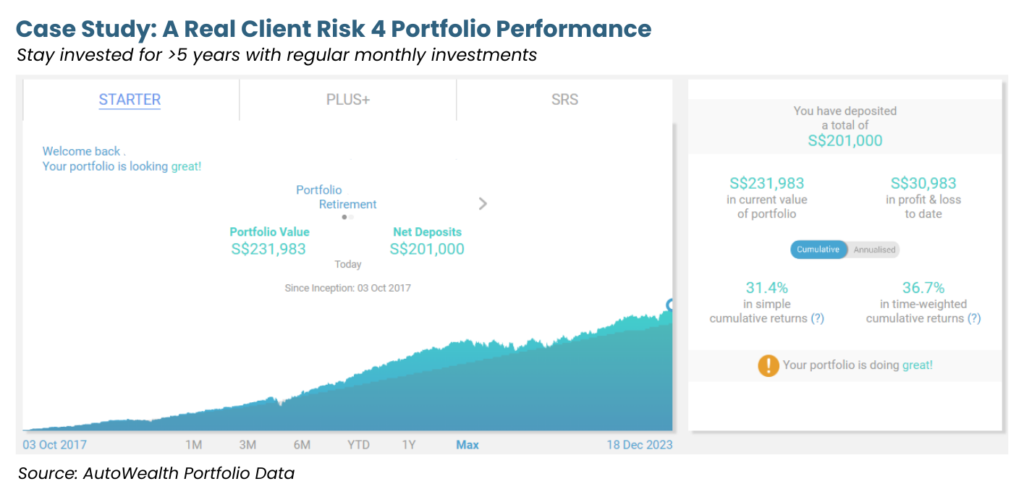

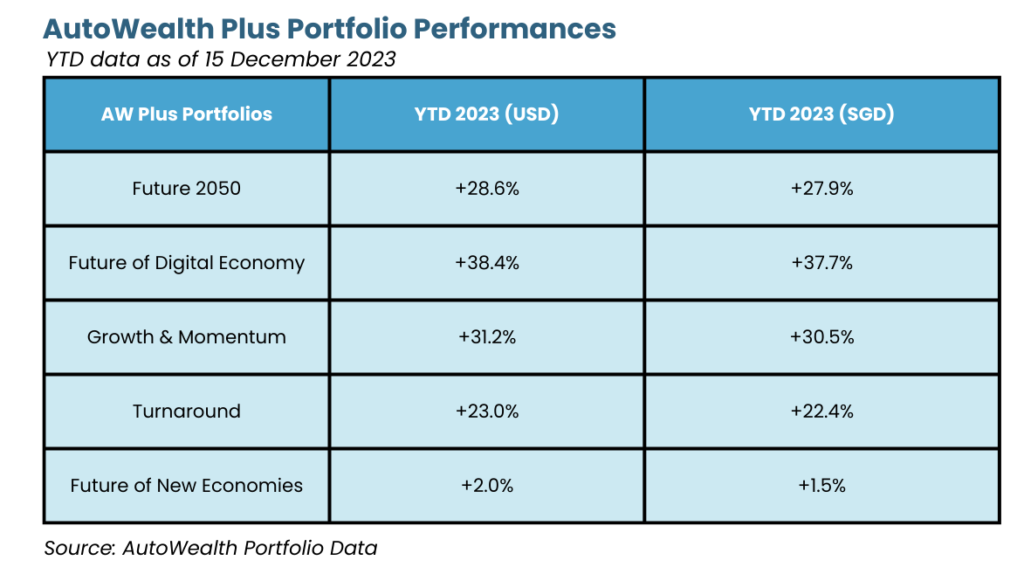

How did our portfolios perform in 2023?

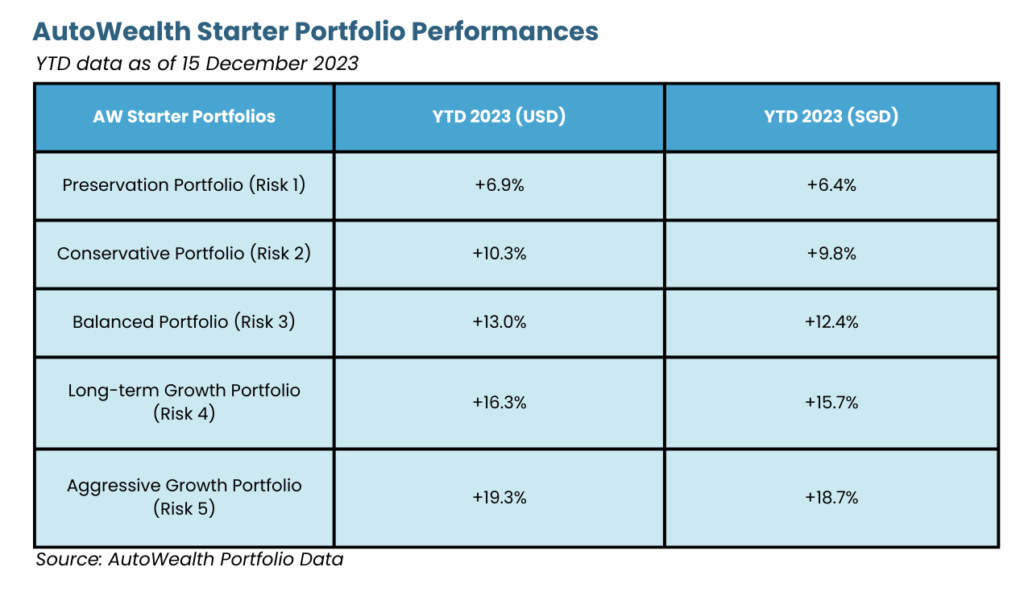

Despite a bumpy 2023, our AutoWealth portfolios rebounded strongly and delivered solid returns as of 15 December 2023.

Our AutoWealth Starter Portfolios generated positive returns in the range of 6.9% to 19.3%, with portfolios on the higher risk spectrum (Risk 3, 4 & 5) achieving double digit returns this year.

With the exception of Future of New Economies delivering a modest return of 2.0%, primarily dragged by China’s weakness, the AutoWealth Plus+ Portfolios delivered stellar double digit returns this year.

Time in the market is more important than timing the market

Have you missed out on our investment calls? Fret not – as time in the market is always more important than timing the market!

It is extremely difficult to consistently time the market correctly and as such, we urged investors to take a long-term view and exercise dollar-cost averaging (DCA) diligently to build long-term wealth. The portfolio below could be yours as well!