🧧🧧The auspicious time for saving & investing is here! Check out what is LiChun and how you can fully capitalise on it Learn More →

Save Smarter For Retirement: Exploring SRS

July 11, 2024

Save Smarter For Retirement: Exploring SRS

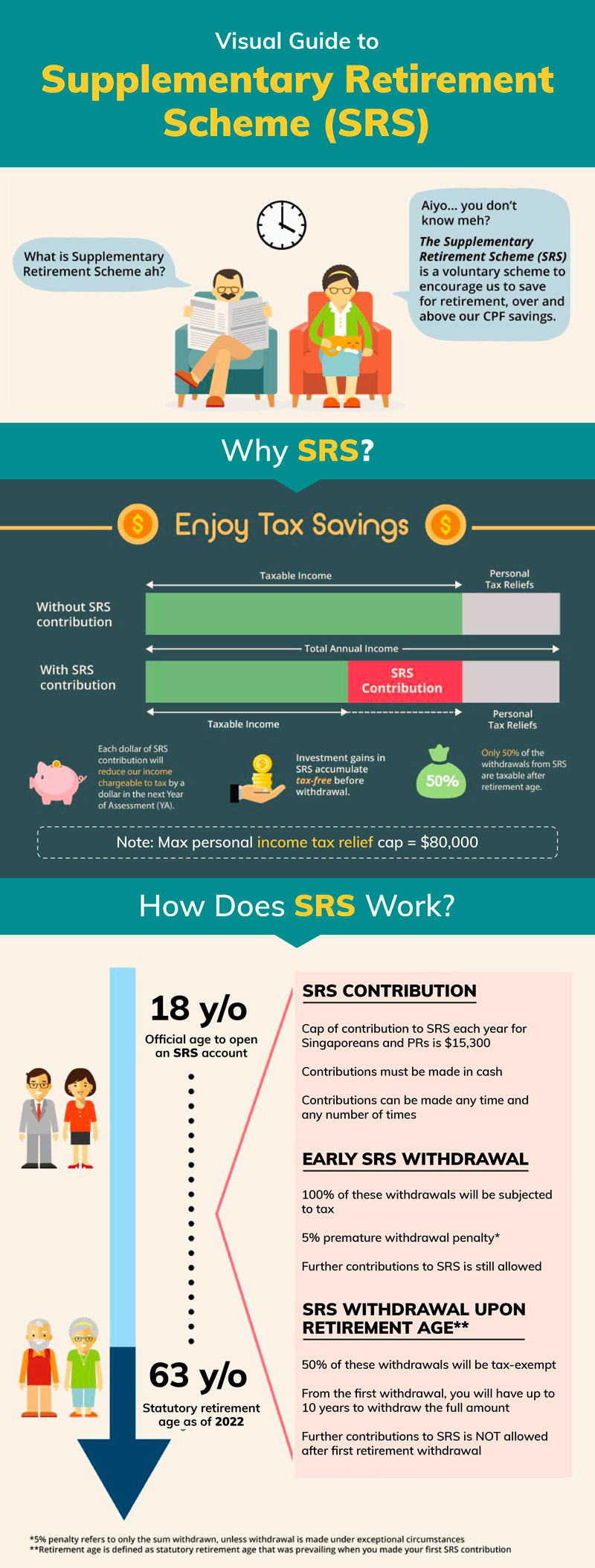

You might have heard about the 1M65 movement where individuals aim to save S$1 million by the time they’re 65 to cover their retirement needs. Many Singaporeans depend on their CPF savings for retirement, but CPF payouts might not be enough since they’re only designed to provide a basic income. This is why you should utilise the Supplementary Retirement Scheme (SRS) to complement your retirement strategy.

What is SRS?

SRS is a voluntary savings scheme that helps you grow your retirement funds on top of your CPF savings. It offers tax relief on your contributions, making it a great choice for Singaporean Citizens, Permanent Residents and Foreigners above the age of 18 years old. You can use your SRS contributions to purchase various investment products, and any returns you earn are tax free!

How does SRS work?

Open a SRS account with any of the 3 banks: DBS, OCBC or UOB

Start your contributions by 31 Dec to get SRS tax relief for the next Year of Assessment. You can put in up to $15,300 a year if you’re a Singapore Citizen or Permanent Resident and up to $35,700 if you’re a foreigner

Now, the bank will provide the contribution details with IRAS and your tax relief will show up in the next Year of Assessment

Note: You can withdraw from your SRS account when you turn 63 (effective from 1 Jul 2022) if you’re a Singaporean or Permanent Resident. For foreigners, you can withdraw after a minimum of 10 years from your first contribution. The plus point is that you can enjoy a 50% tax concession on your withdrawals (i.e. only 50% of the withdrawal is subject to tax). Early withdrawals are subjected to a 5% penalty fee.

Importance/ Benefits of SRS

Why is SRS important? With SRS, you can hedge against inflation through:

1. Tax savings

Did you know that investment returns are accumulated tax-free? Apart from that, contributions to SRS are eligible for tax relief and you get to enjoy 50% tax concession on your withdrawals!

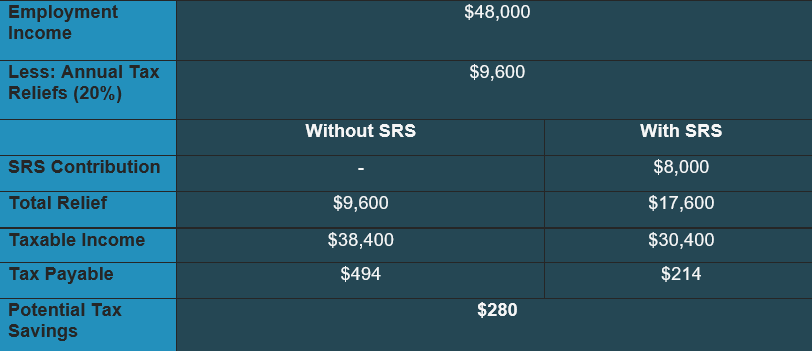

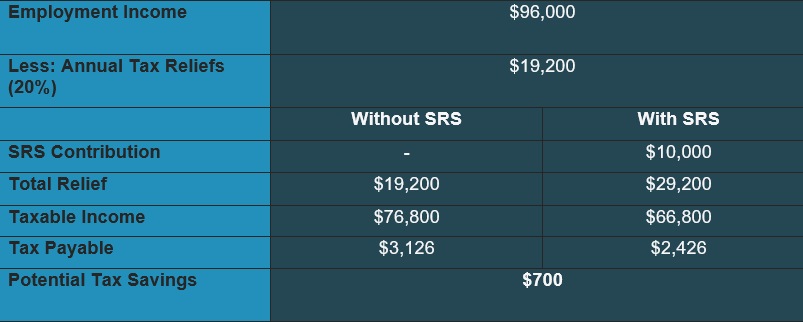

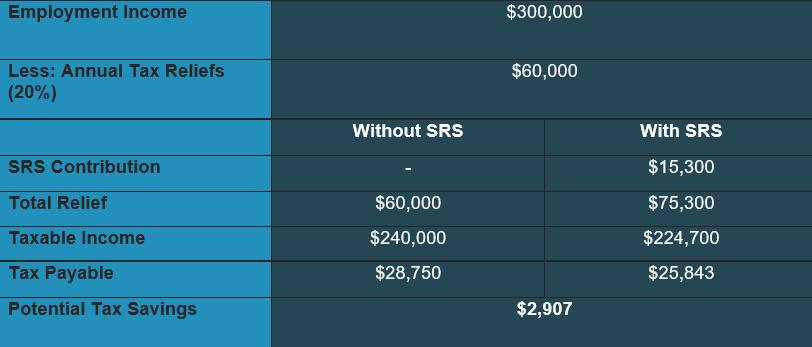

Whether you earn a median income ($48,000 annually), high income ($96,000 annually) or accredited investor income ($300,000 annually), you can save on taxes with SRS.

We’ve included examples of SRS tax savings for median income earners, high income earners and accredited investor below:

Note: Assuming you receive 20% annual tax reliefs, 80% of your income is still subjected to taxes. Tax Payable are calculated based on IRAS tax rates.

Median Income ($48,000 annually)

High Income ($96,000 annually)

Accredited Investor ($300,000 annually)

2. Maximize your investments

Why let your SRS funds earn only 0.05% p.a. in a SRS account? By investing your SRS funds, you can potentially get much better returns. Plus, investment returns are tax-free, allowing you to accumulate your wealth faster.

Diversification is key! There are many forms of investment to help you diversify your portfolio and avoid unnecessary risks: endowment insurance plans, unit trusts, shares or Exchange Traded Funds (ETF), Singapore Government Securities and Robo-Advisors.

Conclusion

Looking to maximize your retirement savings and hit the 1M65 goal? You can enjoy significant tax reliefs on your SRS contributions and build a diversified investment portfolio to see higher returns. Explore Autowealth SRS today to find out more about how we can help you achieve your retirement goals with a well-planned and diversified retirement strategy!